More jobs, less health insurance

Industries offering few or no benefits remain biggest contributors to job growth

Today’s positive jobs report raises anew the issue I discussed two weeks ago when the Biden administration announced a record enrollment in Obamacare plans for 2023. That issue is the steady erosion of employer-based health insurance.

The good news is that job growth rose at a hefty pace in January with the economy adding 517,000 jobs, significantly more than the 401,000 monthly new jobs it averaged during 2022. The unemployment rate of 3.4% was unchanged, but remains at the lowest level recorded since 1969.

But what industries are growing fastest? The top job gainer was leisure and hospitality with 128,000 new jobs; next was food services and drinking places with 99,000 new jobs. Add in the 30,000 new jobs at retailing establishments, 23,000 new jobs in transportation and warehousing, and 17,000 jobs in nursing and residential care facilities, and you get 57% of all new jobs came in industries where the average pay is well below the national median wage of $54,000 per year.

Many of the jobs in these industries do not provide health insurance. Or, if the employers offer it, they have the lowest take-up rates among employees because of high out-of-pocket costs for their workers in the form of co-premiums, co-pays and deductibles.

The result is a continuation of the long-term trend of stagnation in the total number of people with employer-based health insurance (currently about 60% of anyone with health insurance). There were still 27 million Americans uninsured in 2021, according to the Census Bureau’s latest annual survey, which was 2 million more than when President Obama left office and an 8% uninsured rate.

The Affordable Care Act has picked up some of the falloff in employer-based coverage by subsidizing low-wage workers buying Obamacare plans. The ACA’s Medicaid expansion, which provides covers people earning up to 138% of the federal poverty level, contributed even more.

However, 11 states still have not expanded Medicaid. They include Texas (uninsured rate of 18%) and Florida, Georgia, Wyoming and Oklahoma, all with uninsured rates at 12% or above.

No solutions in sight

With Sen. Bernie Sanders (I-VT) taking over the Health Education Labor and Pensions Committee in the Senate, the talk in Washington has turned to possible solutions. Some Democrats are pushing to revive creation of a public option “default” plan for anyone without insurance, an approach rejected by a Democratically-controlled Senate in 2010 when the ACA passed. It would stand no chance of passage now since Republicans control the House.

Sanders recognizes that fact. In an interview with Vermont Public this week, he said he had no plans to turn the committee into a forum for pushing bills that stand no chance of passage in the House — or even the Senate like his cherished Medicare for All bill. “We don't have the votes in the Senate to pass it right now. But what I do hope that we can move forward, maybe in a bipartisan way, is expanding primary health care," Sanders said.

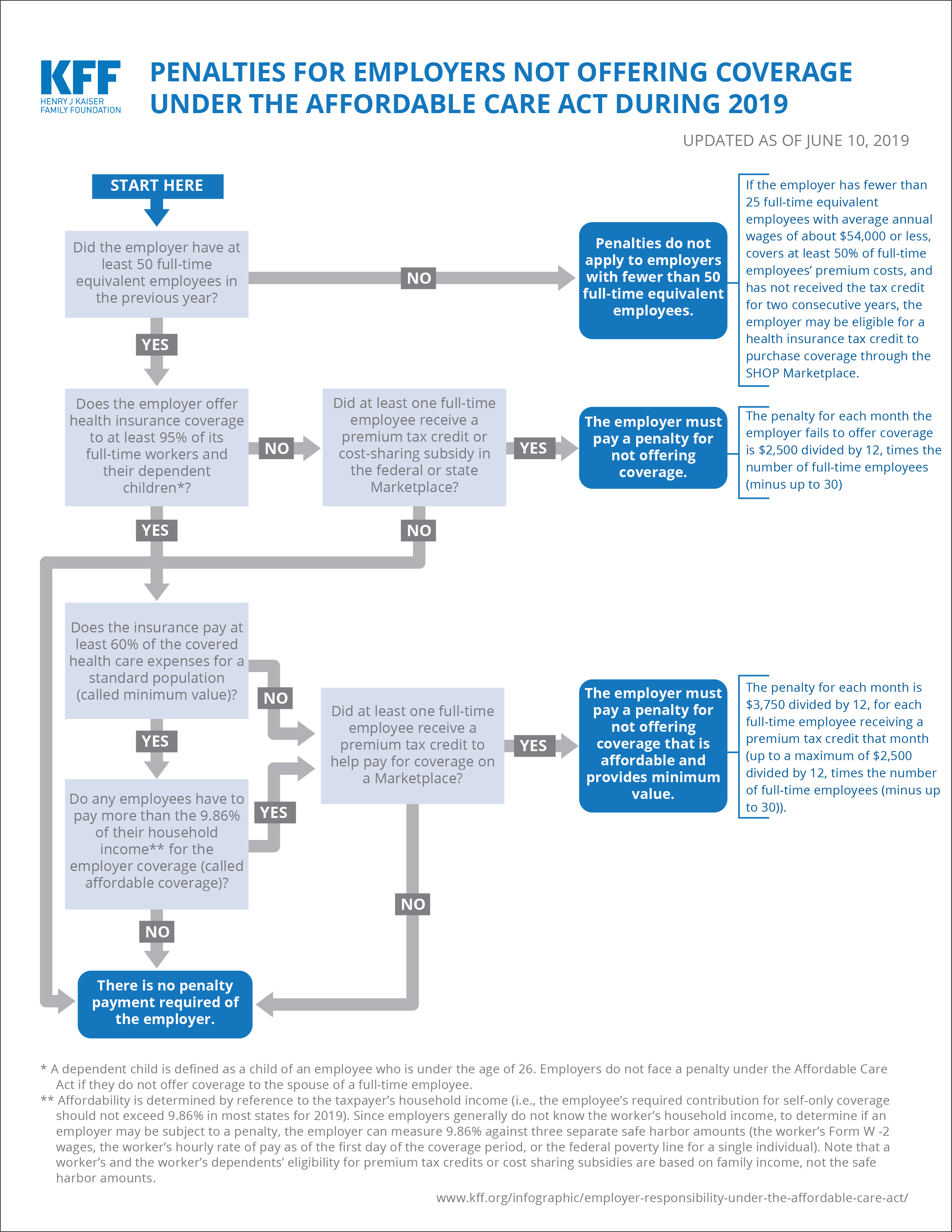

Here’s a suggestion: He might want to hold hearings on the employer mandate in the ACA and investigate why the penalties for non-coverage have not incentivized more low-wage employers to provide coverage. Most of them are small businesses (over 80% of business with fewer than 100 employees provide health coverage).

They’d obviously rather pay the small penalties for non-coverage ($2,500 per year for any worker who individually buys coverage on an Obamacare exchange) than pay for premiums for individuals that now average nearly $8,000 per year.

{kind=link}

So is that a good idea — to encourage low-wage employers to spend the equivalent of the penalty (which could be adjusted up) — to subsidize the upfront costs of an exchange plan? You could also offer those employees a government-run program to counsel employees on the best plans for their needs. That could be financed by a very small surcharge on all premiums.

It could be that employers offering crappy insurance to low-wage workers is a worse problem than offering none at all. An employer offer of insurance deemed "affordable" by ACA standards disqualifies the employee from subsidies in the ACA marketplace, whereas a lot of low income workers can get decent coverage in the marketplace if they're not disqualified in that way.

One unknown at this point is the extent to which employers are taking up the Trump admin-initiated option to subsidize marketplace coverage for their employees and satisfy the employer mandate that way. HealthSherpa, the dominant commercial e-brokerage processing ACA marketplace enrollments (mostly through brokers) claimed last July that its processing of employer-sponsored enrollments was up tenfold, albeit from an unspecified and probably very low starting point. https://www.businesswire.com/news/home/20220718005114/en/Alegeus-and-HealthSherpa-Experience-Significant-Momentum-for-ICHRA